Depreciation, also referred to as a capital allowance, is intended to represent the declining value of an asset. A portion of the asset cost is claimed as depreciation expense. The balance remaining, or written down value, is left to claim in future years, if eligible.

The Australian Taxation Office (ATO) produces a guide each year determining the effective life of a large variety of assets. This guide takes the form of a tax ruling.

The effective life is just that; the expected life of an asset.

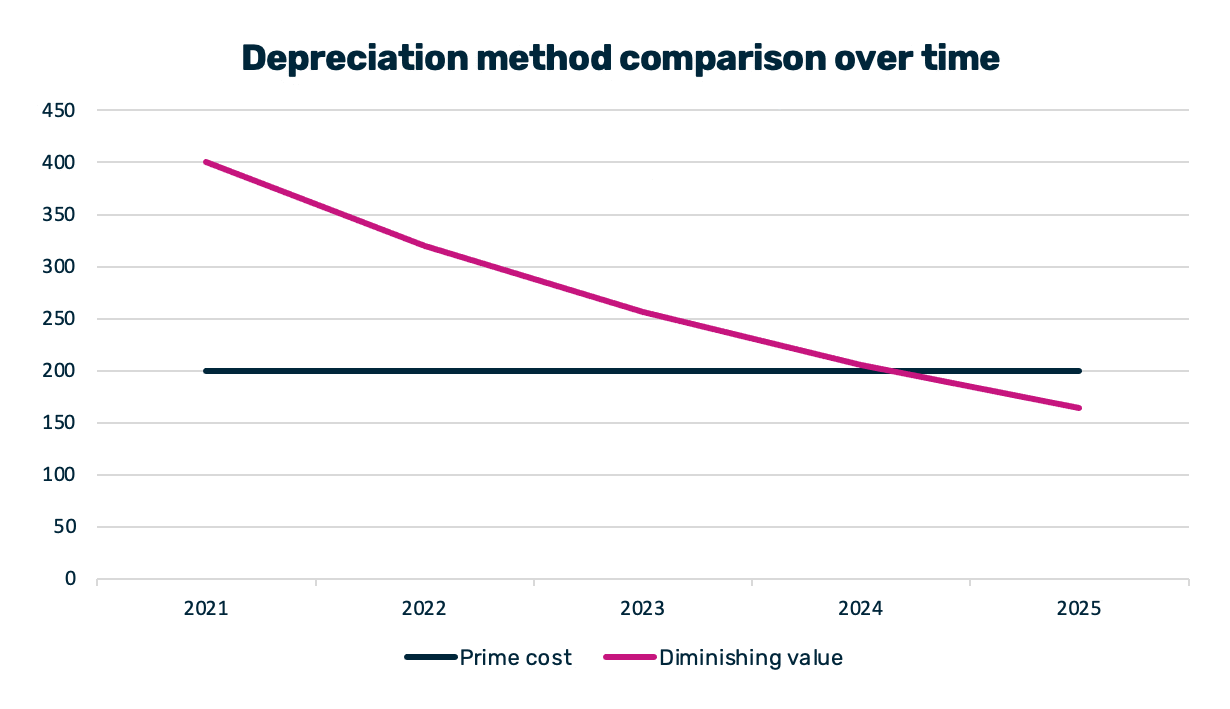

The next step after finding the appropriate effective life is to decide which of two depreciation methods to adopt. The differences between the straight line (prime cost) and diminishing value methods are represented in the table below.

It is important to remember that either way, the expense or deduction available is limited to the total cost of the asset. The only thing that changes is when the deduction is claimed.

If you are claiming depreciation, it is important to regularly review your depreciation schedule to ensure that the items you are claiming still exist and are still deductible (i.e. still used for income-producing purposes).

Now let’s talk "simplified depreciation" and who can use it.

We will categorise the “who” into three main groups:

- Employees claiming depreciation on tools or equipment used at their job.

- Investors claiming depreciation on equipment purchased for rented properties.

- Small businesses.

Low-value pools (LVP) are able to be used by all three groups. Assets must be $1,000 or less, including GST.

Small business general pools (general pool) may be used where the business meets the small business criteria. Predominantly this means annual income before deducting expenses (or turnover) of less than $10 million.

Immediate write off concessions.

This is really in two parts.

- Part A is for groups 1 & 2. Employees and investors (predominantly individuals) can claim an immediate deduction for assets under $300.

- Part B is relevant to group 3, small businesses. This deduction relief is also not limited to small businesses, any business with a turnover of up to $500 million. Larger businesses call it temporary full expensing rather than instant asset write off.

See the table below for calculation methods for simplified depreciation and who can use it.

| Year 1 | Year 2 | Employees | Rentals | Business | |

|---|---|---|---|---|---|

| Low-value pool (LVP) | 18.75% | 37.5% | Y | Y | Y |

| General pool | 15% | 30% | n/a | n/a | Y |

| Immediate write off | 100% | Y - $300 | Y - $300 | Y - $30,000 |

Disclaimer: Information is correct as of April 2022.